A Home Equity Line of Credit (HELOC) is a flexible type of loan that allows homeowners to borrow against the equity they have built up in their property, using that equity as collateral to secure the credit line.

Unlike a standard loan that provides a fixed amount upfront, a HELOC functions more like a revolving credit account, giving borrowers the ability to access funds as needed within an approved limit..

Benefits of HELOC program

- Access cash when you need it

- Lower interest rates than credit cards or personal loans

- Only pay interest on what you use

- Potential to increase your home’s value with smart improvements

- Flexible repayment options for your lifestyle

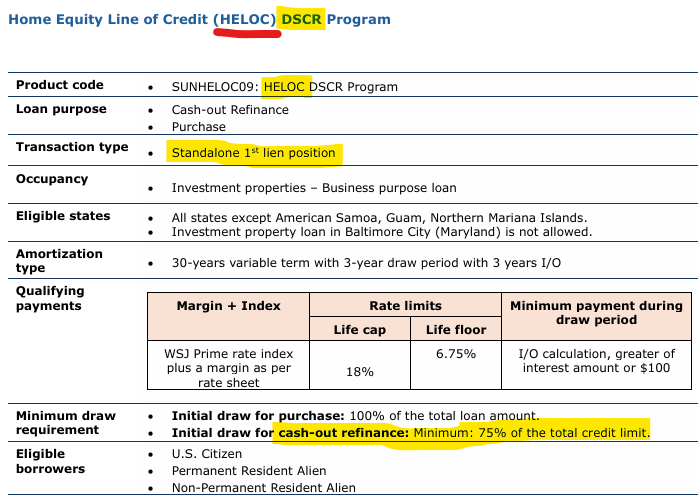

DSCR HELOC

A Debt Service Coverage Ratio (DSCR) Home Equity Line of Credit (HELOC) is a financial product tailored specifically for property investors – seasoned and first-time investors eligible. DSCR HELOC allows investors to leverage their rental income to secure a revolving line of credit.

DSCR HELOC program details:

- Maximum loan amount: $3 million

- Qualifying income is the subject property’s DSCR*

- Minimum FICO: 700

- 30-year variable term with 3-year draw period

- No minimum DSCR

- Maximum Loan-to-Value (LTV): 75%

- First-time investors allowed

- Eligible properties: 1-4 unit properties, Planned Unit Developments (PUDs), warrantable condominiums

- Vesting in the name of Limited Liability Company (LLC), partnership, and corporations allowed

- The maximum number of borrowers allowed per loan is four (4)

HELOC Program benefits:

- Borrow against your investment property’s equity with ease.

- Qualify based on property income, not personal income.

- Flexible revolving line of credit.

- Competitive variable interest rates with interest-only payment options.

- Supports short-term rental and other income-generating properties.

- Access funds for renovations, new investments, or other business opportunities.

- Simple approval process designed for real estate investors.

Eligibility for 1st Lien HELOC:

- Minimum DSCR ≥ 0.75

- Loan Amount: $2,000,001 – $3,000,000

- FICO: 760

- LTV/CLTV: 75%

- Reserve Requirement: 6 months

- Loan Amount: $750,001 – $2,000,000

- FICO: 720

- LTV/CLTV: 75%

- Reserve Requirement: 6 months

- Loan Amount: $50,000 – $750,000

- FICO: 720

- LTV/CLTV: 75%

- Reserve Requirement: 6 months

- Loan Amount: $50,000 – $750,000

- FICO: 700

- LTV/CLTV: 70%

- Reserve Requirement: 6 months

- Loan Amount: $2,000,001 – $3,000,000

- No Minimum DSCR

- Loan Amount: $2,000,001 – $3,000,000

- FICO: 760

- LTV/CLTV: 75%

- Reserve Requirement: 12 months

- Loan Amount: $50,000 – $2,000,000

- FICO: 720

- LTV/CLTV: 75%

- Reserve Requirement: 12 months

- Loan Amount: $50,000 – $750,000

- FICO: 700

- LTV/CLTV: 70%

- Reserve Requirement: 9 months

- Loan Amount: $2,000,001 – $3,000,000

Note: Cash out proceeds can’t be used for reserve requirements.

DSCR documentation:

- Long Term rental documentation:

- FNMA Form 1007 or 1025 reflects long-term market rents.

- Executed Lease agreement.

- Short-term rental (e.g., Airbnb, VRBO, Flip Key) documentation:

- A 5% LTV reduction applies to all transactions using short-term rental income.

- FNMA Form 1007 or 1025 reflecting short-term market rents.

- The most recent 24-month bank statements from the borrower evidence short-term rental deposits. The borrower must provide rental records for the subject property to support monthly deposits.

- Gross rents must be reduced by 20% to reflect extraordinary costs (i.e., advertising, furnishings, cleaning) associated with operating short-term rental property.